Underwriting Signals Shaping Flood, Specialty Property & Fine Art Insurance

The insurance landscape entering 2026 is shaped by rising loss trends, shifting risk perceptions, and rapidly evolving client needs across flood, specialty property, and fine art. Despite a quiet 2025 hurricane season, flood exposure remains severe, with catastrophic floods in the U.S. averaging about $4.5 billion per event.

Widespread underinsurance driven by rising construction costs, misconceptions about coverage, and outdated flood modelling, has left many homeowners and business owners exposed.

Widespread underinsurance driven by rising construction costs, misconceptions about coverage, and outdated flood modelling, has left many homeowners and business owners exposed.

With several lapses in the National Flood Insurance Program and heightened winter flood risk, proactive education on private market solutions is critical.

Specialty property markets continue to experience volatility fueled by economic uncertainty, high commercial vacancies, maturing real estate debt, and escalating weather‑related losses. Underwriters are cautious, particularly with older properties and high‑risk zones, making strong carrier partnerships and demonstrated risk‑reduction essential for clients.

Meanwhile, the fine art market is undergoing an evolution as generational wealth transfer accelerates interest in alternative collectibles and introduces new valuation and security challenges. Increasing catastrophe exposures, cyber threats, and digital title vulnerabilities are prompting tighter underwriting and demand for innovative, customized coverage.

Across all segments, brokers and agents must lean on data, technology, and experienced carrier partners to close protection gaps, navigate market uncertainty, and safeguard clients’ assets in an increasingly complex risk environment.

Learn how Tokio Marine Highland can help you better educate clients on flood, property and fine arts risks, and ensure they have adequate coverage to remain resilient long into the future.

Source:

National Centers for Environmental Information, “Billion-Dollar Disasters: Calculating the Costs,” accessed January 22, 2026.

Outdated risk perceptions, NFIP lapses, and the rising frequency and severity of flood risks make 2026 a pivotal time for starting proactive coverage conversations.

The private flood insurance market is entering 2026 with strong momentum, driven by advanced modeling capabilities, abundant capacity, and a quiet hurricane season in 2025. However, that lull in Atlantic storm activity is not indicative of future risk. In fact, the disconnect between perceived and actual flood exposure is significant, with many home and business owners underestimating their vulnerability. This gap, combined with rising construction costs and economic uncertainty, underscores the importance of proactive risk management and adequate coverage.

Weather-related water losses rose 25.4% from 2023 to 2024, with the cost of each significant flood event in the U.S. averaging $4.5 billion.

Floods are the most common natural disaster in the United States, and more than 99% of U.S. counties experienced a flood event over the past 20 years. About 20% of all flood claims occur in hazard zones where lenders do not require flood coverage.

Floods are the most common natural disaster in the United States, and more than 99% of U.S. counties experienced a flood event over the past 20 years. About 20% of all flood claims occur in hazard zones where lenders do not require flood coverage.

Misunderstanding and Underestimating Flood Risk

Flood insurance has been available for more than 70 years, yet a troubling divide remains between homeowners’ perception and the actual protection they have against floods in their primary insurance. About a third of U.S. homeowners claim they are protected in the event of a flood, yet just 4% maintain a flood policy. A significant number of business owners are also unaware that flood damage is generally not covered by commercial property policies — including Commercial Package Policies (CPPs) and Business Owners Policies (BOPs), unless specifically endorsed.

Rebuilding after a flood is more expensive and time-consuming than ever, yet few homeowners have increased their coverage to match higher replacement costs — which could leave two out of three households at risk of being underinsured in the event of a disaster. Without adequate coverage, homeowners and business owners face significant out-of-pocket expenses for rebuilding, temporary housing, business interruption costs, and contents.

Outdated flood risk mapping also contributes to the flood insurance gap. Many insurers have increasingly sophisticated modelling and mapping combined with predictive analytics to pinpoint exposures and price risk accordingly. However, federally backed lenders often use criteria from the Federal Emergency Management Agency (FEMA) to manage flood risk, yet many flood-prone properties fall outside FEMA’s Special Flood Hazard areas.

Many homeowners are also unaware of coverage restrictions in their policies or sub-limits that can affect how losses from flood water may be covered.

Many homeowners are also unaware of coverage restrictions in their policies or sub-limits that can affect how losses from flood water may be covered.

The wet winter forecast for 2026 and the heightened risk of flooding due to snowmelt may be one flood insurance conversation starter. Saturated or frozen ground combined with rapid temperature increases can trigger runoff, overwhelm drainage systems, and cause localized flooding, and ice jams further compound these risks. And while 2025 was a historically quiet hurricane season, another inactive season cannot reasonably be expected to continue through 2026.

Capacity in the flood insurance market remains robust, but if an active catastrophe season emerges, rate adjustments and stricter underwriting could follow, making now the time to talk with clients about their flood exposures. In addition, multiple pauses to the National Flood Insurance Program present a risk. While Congress ended the federal flood program shutdown in November after a 43-day hiatus and a subsequent three-day pause in February, future lapses could once again leave home and business owners unable to renew NFIP policies or make changes.

Provide Flood Coverage Comparisons for Clients

Education on flood risk is key, and agents and brokers must bridge the awareness gap and encourage proactive purchasing before catastrophe strikes. Policyholders that currently rely on the NFIP may want to consider the private flood market, where the environment favors proactive buyers who secure coverage before market hardening occurs. Unlike government-backed programs, private flood insurers also offer replacement cost coverage, additional living expenses (ALE), and business interruption options, providing more comprehensive protection. And the private market’s more robust data analytics and modeling tools to precisely assess risk can result in more competitive pricing.

With climate volatility, economic pressures, and regulatory shifts on the horizon, it’s imperative to work with a private flood insurer who offers flexible, customized coverage, and the financial protection clients need to weather any storm.

Sources:

LexisNexis, “2025 LexisNexis U.S. Home Trends Report,” October 23, 2025.

Federal Emergency Management Agency, “Unexpected Flood Risks in Your Community: The Natural & Manufactured,” July 2025.

First Street, “Understand the differences between FEMA flood zones,” accessed January 1, 2026.

Insurance Business, “Survey shows widespread underinsurance among U.S. homeowners,” December 12, 2025.

Bloomberg, “LA Fire Survivors Got a Rude Surprise That Could Hit More Americans,” January 1, 2026.

Moving Day, “Zillow’s climate risk reversal looks like a setback. It’s really a wake-up call,” December 3, 2025.

Moody’s, “Why does the U.S. flood insurance gap persist, and how can private insurance transform the market?” December 3, 2025.

Vacancies, debt maturities, and severe weather are colliding in 2026, creating a volatile specialty property market.

The specialty property insurance market in 2026 will continue to experience volatility, shaped by economic uncertainty, digitization trends, and evolving risk exposures. While 2025 saw a relatively quiet catastrophe season, external factors such as rising construction costs, high borrowing rates, and litigation pressures remain significant drivers of rate fluctuations. These influences have created a market that feels highly unstable — with sudden swings and unpredictable pricing patterns — especially in lender-placed insurance.

While capacity in the overall property market is abundant, commercial property vacancies and elevated interest rates continue to pose challenges for the specialty property market.

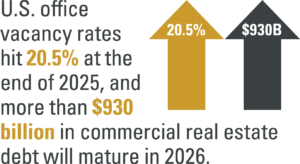

U.S. office vacancy rates hit 20.5% at the end of 2025, and more than $930 billion in commercial real estate debt (CRE) will mature in 2026. Investors who locked in pandemic-era or pre-pandemic interest rates could see their new debt payments rise by 30% or more as the average interest rate on CRE loans rises nearly 2% on maturing debt. Those with office space still abandoned from COVID-19 who haven’t already been pushed to alternative insurance markets or lender-placed programs may see non-renewals as primary insurers pass on covering such properties.

However, industry experts are cautiously optimistic that vacancies will slowly begin to trend downward again in the U.S., and that potential interest rate cuts could benefit investors and trigger refinancing waves.

However, industry experts are cautiously optimistic that vacancies will slowly begin to trend downward again in the U.S., and that potential interest rate cuts could benefit investors and trigger refinancing waves.

Risk Complexity and New Exposure

Brokers and agents face increasing complexity in helping their clients manage risk exposure. Weather patterns remain volatile, and aging infrastructure adds to vulnerability. While newer, well-maintained properties are easier to insure, older buildings present growing challenges.

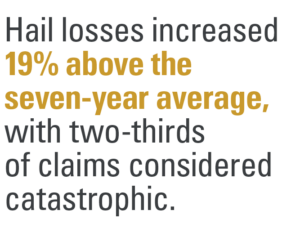

Despite the calm hurricane season, insured losses from convective storms in the U.S. have exceeded $50 billion each of the past three years. Wind claim severity rose nearly 24% in 2024 compared to the prior year, and loss costs jumped by more than 30%. Hail losses also increased 19% above the seven-year average, with two-thirds of claims considered catastrophic.

The California Palisades and Eaton fires in January 2025 also led to significant insured losses totaling $40 million, erasing more than $8 billion in home value.

Building material costs have risen consistently since the pandemic, though the pace has slowed considerably in the past two years. And a lack of experienced construction services workers will cause further delays in projects, further driving up the cost of construction and rebuilding.

Political risk and civil unrest also loom as concerns for certain property segments, particularly those tied to cultural institutions or high-profile commercial assets. Carriers will likely clarify exclusions and may offer coverage enhancements to address these emerging exposures.

Political risk and civil unrest also loom as concerns for certain property segments, particularly those tied to cultural institutions or high-profile commercial assets. Carriers will likely clarify exclusions and may offer coverage enhancements to address these emerging exposures.

Additionally, the auto market — often a leading indicator for lender-placed trends — remains volatile, with high valuations expected to peak and then decline.

With the chaotic market and continued threats from natural catastrophes, underwriters will continue to carefully scrutinize property in high-risk zones. Brokers and agents will need to work with clients on loss prevention and seek out carriers that recognize the value of risk-reduction efforts and price accordingly.

Building relationships to protect value

In this volatile and evolving market, brokers and agents should seek out insurance partners with experience and expertise in the specialty property market, and also those who can leverage evolving technologies while retaining personalized service.

Specialty property insurance in 2026 will be shaped by economic uncertainty, technological acceleration, and evolving risk landscapes. Meeting the needs of clients will require brokers and agents to find partners that embrace digitization, innovate around vacancy and lender-placed challenges, and deliver exceptional service.

Sources:

Cushman & Wakefield, “U.S. Office Reports,” January 2026.

CRE Daily, “Maturing Debt Drives 2026 CRE Distress,” November 18, 2025.

Moody’s, “If a tree falls in the forest: Overcoming challenges in U.S. severe convective storm observations,” November 25, 2025.

LexisNexis, “2025 LexisNexis U.S. Home Trends Report,” October 23, 2025.

Realtor, “True Cost of 2025 Los Angeles Wildfire Emerges a Year After the Disaster,” January 5, 2026.

The fine art marketplace is undergoing a transformation led by a significant generational wealth transfer, a shift in collector behavior, and new and evolving risks.

The fine art insurance market in 2026 is poised for significant transformation, driven by shifting collecting habits, heightened risk awareness, and technological advances. While traditional art remains a cornerstone for fine art insurance, the definition of “collectible” is expanding and shifting toward commoditization.

High-net-worth individuals and younger generations are gravitating toward luxury and alternative assets — watches, classic cars, handbags, sneakers, and rare trading cards. With the so-called Great Wealth Transfer of nearly $124 trillion in assets expected to move from Baby Boomers to their children by 2048, fine art brokers are likely to see the heirs to estates redirecting funds from older fine art collections to new interests.

Both Generation X and Gen Z are more inclined to invest in alternative collectibles, creating unique risk profiles that will require brokers and carriers to develop products that address new valuation dynamics and storage, security, and liquidity considerations.

![]() Emerging trends and risks in 2026

Emerging trends and risks in 2026

While the property insurance market as a whole is softening, underwriting standards for fine art continue to tighten in high-risk zones prone to wildfires, floods, and hurricanes, and underwriters are likely to remain selective and require more risk mitigation and security protocols. Increased replacement costs, along with the growing trend toward the commoditization of art, will make high-value collections more difficult to place. As more collectors leverage paintings, sculptures, and luxury assets for financing, brokers must identify carriers capable of supporting solutions that factor in valuation volatility, lending requirements, and collateralization risks.

Technological advances are also creating new risks for fine art. Blockchain-powered platforms offering digital titles for art and collectibles are creating new vulnerabilities in title security. Digital titles may be stolen, with ownership transferred and resulting in a loss, even if the physical valuable is secure and unharmed.

Technological advances are also creating new risks for fine art. Blockchain-powered platforms offering digital titles for art and collectibles are creating new vulnerabilities in title security. Digital titles may be stolen, with ownership transferred and resulting in a loss, even if the physical valuable is secure and unharmed.

Other risks include the uptick in social engineering used by hackers to impersonate dealers and collectors to divert payment for pieces. Additional threats include shipment interception, redirection schemes, and ransomware targeting digital art. These trends will require brokers and their carrier partners to think outside of the box and look at cyber and fraud solutions to ensure fine art and collectibles clients are fully protected.

Political risk is also gaining attention among galleries and museums, with concerns about civil unrest, insurrection, and government seizure exclusions. Brokers need to ensure they understand all terms of coverage for these risks and explore solutions for these exposures.

Good partners will be key to protection

In 2026, fine art insurance will be defined by agility, innovation, and relationships. Service excellence will remain a key differentiator, and brokers and galleries need to work with underwriting partners able to design creative and customized policies, expedite policy issuance, and provide top-tier service. As wealth transfers accelerate and collecting habits evolve, brokers will need carriers able to adapt their underwriting strategies to protect clients in a market where art is not just a passion — it’s an asset class.

Sources:

New York Times, “The Greatest Wealth Transfer in History Is Here, With Familiar (Rich) Winners,” May 14, 2023.

Artsy, “5 Art Scams Every Art Buyer Should Know — and How to Avoid Them,” August 18, 2025